As filed with the Securities and Exchange Commission on June 24, 2009

Registration No.

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-4

REGISTRATION STATEMENT

UNDER THE

SECURITIES ACT OF 1933

TWO HARBORS INVESTMENT CORP.

(Exact Name of Each Registrant as Specified in Its Charter)

| Maryland | 6798 | 27-0312904 | ||

| (State or Other Jurisdiction of Incorporation or Organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

| 601 Carlson Parkway, Suite 330 Minnetonka, MN 55305 (612) 238-3300 |

Brian C. Taylor, Chairman Two Harbors Investment Corp. 601 Carlson Parkway, Suite 330 Minnetonka, MN 55305 (612) 238-3300 | |

| (Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices) |

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent for Service) |

Copies to:

| David Alan Miller, Esq. Jeffrey M. Gallant, Esq. Graubard Miller The Chrysler Building 405 Lexington Avenue New York, New York 10174 Telephone: (212) 818-8800 Fax: (212) 818-8881 |

Brian Hoffmann, Esq. Jay Bernstein, Esq. Clifford Chance US LLP 31 West 52nd Street New York, New York 10019 Telephone: (212) 878-8000 Fax: (212) 878-8375 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective and all other conditions to the merger contemplated by the merger agreement described in the included proxy statement/prospectus have been satisfied or waived.

If the securities being registered on this form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box: ¨

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer ¨ | |

| Non-accelerated filer x | Smaller reporting company ¨ | |

| (Do not check if a smaller reporting company) |

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

Exchange Act Rule 13e-4(i) (Cross-Border Issuer Tender Offer) ¨

Exchange Act Rule 14d-1(d) (Cross-Border Third-Party Tender Offer) ¨

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Security Being Registered(1) |

Amount Being Registered |

Proposed Maximum Offering Price per Security(2) |

Proposed Maximum Aggregate Offering Price |

Amount of Registration Fee(3) | |||||||

| Shares of common stock(4) |

26,249,000 | $ | 9.69 | $ | 254,352,810 | $ | 14,192.89 | ||||

| Warrants to purchase shares of common stock(4) |

33,249,000 | $ | 0.47 | $ | 15,627,030 | $ | 871.99 | ||||

| Shares of common stock underlying the Warrants(4)(5) |

33,249,000 | $ | 9.69 | $ | 322,182,810 | $ | 17,977.80 | ||||

| Total Fee Due |

$ | 592,162,650 | $ | 33,042.68 | |||||||

| (1) | All securities being registered are to be issued by Two Harbors Investment Corp., a Maryland corporation (“Two Harbors”). In connection with the merger of Capitol Acquisition Corp. (“Capitol”), a publicly-traded Delaware corporation, and Two Harbors Merger Corp., as described in the proxy statement/prospectus forming a part of this registration statement, all of the outstanding common stock of Capitol held by public stockholders and all of the outstanding warrants of Capitol held by public and private warrantholders will be converted on a one-for-one basis into securities of Two Harbors. As a result of the merger and related transactions, Capitol will become a subsidiary of Two Harbors. |

| (2) | Based on the prices on June 18, 2009 of the common stock and warrants of Capitol pursuant to Rule 457(f)(1). |

| (3) | Determined in accordance with Section 6(b) of the Securities Act at a rate equal to $55.80 per $1,000,000 of the proposed maximum aggregate offering price. |

| (4) | Shares of common stock and warrants that will be issued to holders of securities of Capitol upon consummation of the transactions described in footnote 1 above. |

| (5) | Pursuant to Rule 416, there are also being registered such additional securities as may be issued to prevent dilution resulting from stock splits, stock dividends or similar transactions or as a result of the anti-dilution provisions contained in the warrants. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the SEC, acting pursuant to said Section 8(a), may determine.

CAPITOL ACQUISITION CORP.

509 7TH STREET, N.W.

WASHINGTON, D.C. 20004

NOTICE OF SPECIAL MEETING OF STOCKHOLDERS

OF CAPITOL ACQUISITION CORP.

TO BE HELD ON , 2009

To the Stockholders of Capitol Acquisition Corp.:

NOTICE IS HEREBY GIVEN that the special meeting of stockholders of Capitol Acquisition Corp., a Delaware corporation (“Capitol”), will be held at 10:00 a.m. eastern time, on , 2009, at the offices of Graubard Miller, Capitol’s counsel, at The Chrysler Building, 405 Lexington Avenue, 19th Floor, New York, New York 10174. You are cordially invited to attend the meeting, which will be held for the following purposes:

(1) to consider and vote upon a proposal to amend Capitol’s amended and restated certificate of incorporation to allow Capitol to complete the merger with Two Harbors Merger Corp., a Delaware corporation (“Merger Sub Corp.”) and a wholly-owned subsidiary of Two Harbors Investment Corp., a Maryland corporation (“Two Harbors”), even though (i) Capitol will ultimately be acquired by Two Harbors, (ii) neither Two Harbors nor Merger Sub Corp. is an operating business, (iii) the fair market value of Two Harbors and Merger Sub Corp. on the date of the transaction is less than 80% of the balance of Capitol’s trust account and (iv) the transaction will not be approved by disinterested independent directors and (v) Capitol will not be receiving a fairness opinion from an independent investment banking firm that the transaction is fair to public stockholders from a financial point of view — this proposal is referred to as the “initial charter proposal”;

(2) to consider and vote upon a proposal to (i) adopt the Agreement and Plan of Merger, dated as of June 11, 2009, among Capitol, Merger Sub Corp., Two Harbors and Pine River Capital Management L.P., a Delaware limited partnership (“Pine River”) and the sole stockholder of Two Harbors, which, among other things, provides for the merger of Merger Sub Corp. with and into Capitol, with Capitol being the surviving entity and becoming a wholly owned subsidiary of Two Harbors, and (ii) approve the business combination contemplated by such Agreement and Plan of Merger — this proposal is referred to as the “merger proposal”;

(3) to consider and vote upon separate proposals to approve the following differences between the charter of Two Harbors to be in effect following the merger and Capitol’s current amended and restated certificate of incorporation: (i) the name of the new public entity will be “Two Harbors Investment Corp.” as opposed to “Capitol Acquisition Corp.”; (ii) Two Harbors will have 450,000,000 authorized shares of common stock and 50,000,000 authorized shares of preferred stock and may increase or decrease such amounts without stockholder approval, as opposed to Capitol having 75,000,000 authorized shares of common stock and 1,000,000 authorized shares of preferred stock and not being able to increase or decrease such amounts without stockholder approval; (iii) Two Harbors’ corporate existence will be perpetual as opposed to Capitol’s corporate existence terminating on November 8, 2009; (iv) Two Harbors’ board of directors will not be classified as opposed to Capitol’s which is classified; (v) Two Harbors’ charter will not include the various provisions applicable only to specified purpose acquisition corporations that Capitol’s amended and restated certificate of incorporation contains; and (vi) Two Harbors’ charter will include various provisions relating to Two Harbors’ intention to elect and qualify to be taxed as a real estate investment trust (“REIT”) for U.S. federal income tax purposes, commencing with Two Harbors’ taxable year ending December 31, 2009, which are not included in Capitol’s amended and restated certificate of incorporation — we refer to these proposals collectively as the “secondary charter proposals”; and

(4) to consider and vote upon a proposal to adjourn the special meeting to a later date or dates, if necessary, to permit further solicitation and vote of proxies if, based upon the tabulated vote at the time of the special meeting, Capitol is not authorized to consummate the merger — this proposal is referred to as the “adjournment proposal.”

These items of business are described in the attached proxy statement/prospectus, which you are encouraged to read in its entirety before voting. Only holders of record of Capitol common stock at the close of business on , 2009 are entitled to notice of the special meeting and to vote and have their votes counted at the special meeting and any adjournments or postponements of the special meeting.

Capitol’s officers, directors and stockholders prior to Capitol’s initial public offering have agreed to vote any shares of Capitol common stock they purchase after the execution of the merger agreement in favor of the proposals being presented at the special meeting.

After careful consideration, Capitol’s board of directors has determined that the proposals are fair to and in the best interests of Capitol and its stockholders and unanimously recommends that you vote or give instruction to vote “FOR” the approval of all of the proposals.

The approval of the initial charter proposal and the merger proposal is a condition to the consummation of the merger discussed above. Under the merger agreement, the approval of the secondary charter proposals is not a condition to the consummation of the merger and the vote on such proposal will not impact whether the merger is consummated.

All Capitol stockholders are cordially invited to attend the special meeting in person. To ensure your representation at the special meeting, however, you are urged to complete, sign, date and return the enclosed proxy card as soon as possible. If you are a stockholder of record of Capitol common stock, you may also cast your vote in person at the special meeting. If your shares are held in an account at a brokerage firm or bank, you must instruct your broker or bank on how to vote your shares or, if you wish to attend the meeting and vote in person, obtain a proxy from your broker or bank.

A complete list of Capitol stockholders of record entitled to vote at the special meeting will be available for ten days before the special meeting at the principal executive offices of Capitol for inspection by stockholders during ordinary business hours for any purpose germane to the special meeting.

Your vote is important regardless of the number of shares you own. Whether you plan to attend the special meeting or not, please sign, date and return the enclosed proxy card as soon as possible in the envelope provided. If your shares are held in “street name” or are in a margin or similar account, you should contact your broker to ensure that votes related to the shares you beneficially own are properly counted.

Thank you for your participation. We look forward to your continued support.

| , 2009 | By Order of the Board of Directors | |

| Mark D. Ein | ||

| Chairman of the Board | ||

IF YOU RETURN YOUR PROXY CARD WITHOUT AN INDICATION OF HOW YOU WISH TO VOTE, YOUR SHARES WILL BE VOTED IN FAVOR OF EACH OF THE PROPOSALS AND YOU WILL NOT BE ELIGIBLE TO HAVE YOUR SHARES CONVERTED INTO A PRO RATA PORTION OF THE TRUST ACCOUNT IN WHICH A SUBSTANTIAL PORTION OF THE NET PROCEEDS OF CAPITOL’S INITIAL PUBLIC OFFERING (“IPO”) ARE HELD. YOU MUST AFFIRMATIVELY VOTE AGAINST THE MERGER PROPOSAL AND DEMAND THAT CAPITOL CONVERT YOUR SHARES INTO CASH NO LATER THAN THE CLOSE OF THE VOTE ON THE MERGER PROPOSAL TO EXERCISE YOUR CONVERSION RIGHTS. IN ORDER TO CONVERT YOUR SHARES, YOU MUST TENDER YOUR STOCK TO CAPITOL’S STOCK TRANSFER AGENT PRIOR TO THE SPECIAL MEETING OF CAPITOL STOCKHOLDERS. YOU MAY TENDER YOUR STOCK BY EITHER DELIVERING YOUR STOCK CERTIFICATE TO THE TRANSFER AGENT OR BY DELIVERING YOUR SHARES ELECTRONICALLY USING THE DEPOSITORY TRUST COMPANY’S DWAC (DEPOSIT WITHDRAWAL AT CUSTODIAN) SYSTEM. IF THE MERGER IS NOT COMPLETED, THEN THESE SHARES WILL NOT BE CONVERTED INTO CASH. IF YOU HOLD THE SHARES IN STREET NAME, YOU WILL NEED TO INSTRUCT THE ACCOUNT EXECUTIVE AT YOUR BANK OR BROKER TO WITHDRAW THE SHARES FROM YOUR ACCOUNT IN ORDER TO EXERCISE YOUR CONVERSION RIGHTS. SEE “THE MERGER PROPOSAL — CONVERSION RIGHTS” FOR MORE SPECIFIC INSTRUCTIONS.

CAPITOL ACQUISITION CORP.

509 7TH STREET, N.W.

WASHINGTON, D.C. 20004

NOTICE OF SPECIAL MEETING OF WARRANTHOLDERS

OF CAPITOL ACQUISITION CORP.

TO BE HELD ON , 2009

To the Warrantholders of Capitol Acquisition Corp.:

NOTICE IS HEREBY GIVEN that the special meeting of warrantholders of Capitol Acquisition Corp., a Delaware corporation (“Capitol”), will be held at 10:00 a.m. eastern time, on , 2009, at the offices of Graubard Miller, Capitol’s counsel, at The Chrysler Building, 405 Lexington Avenue, 19th Floor, New York, New York 10174. You are cordially invited to attend the meeting, which will be held for the following purposes:

(1) to consider and vote upon a proposal to amend certain terms of the Warrant Agreement, dated as of November 8, 2007, between Capitol and Continental Stock Transfer & Trust Company which governs the terms of Capitol’s outstanding warrants, in connection with the consummation of the transactions contemplated by the Agreement and Plan of Merger, dated as of June 11, 2009, among Capitol, Two Harbors Investment Corp., a Maryland corporation (“Two Harbors”), Two Harbors Merger Corp., a Delaware corporation (“Merger Sub Corp.”) and a wholly-owned subsidiary of Two Harbors, and Pine River Capital Management L.P., a Delaware limited partnership (“Pine River”) and the sole stockholder of Two Harbors, which, among other things, provides for the merger of Merger Sub Corp. with and into Capitol with Capitol being the surviving entity and becoming a wholly-owned subsidiary of Two Harbors. The amendment to the Warrant Agreement will provide that (i) the exercise price of Capitol’s warrants will be increased to $11.00 per share and (ii) the expiration date of the warrants will be extended from November 7, 2012 to November 7, 2013 — this proposal is referred to as the “warrant amendment proposal”;

(2) to consider and vote upon a proposal to adjourn the special meeting to a later date or dates, if necessary, to permit further solicitation and vote of proxies if, based upon the tabulated vote at the time of the special meeting, Capitol is not authorized to consummate the warrant amendment proposal — this proposal is referred to as the “adjournment proposal.”

These items of business are described in the attached proxy statement/prospectus, which you are encouraged to read in its entirety before voting. Only holders of record of Capitol warrants at the close of business on , 2009 are entitled to notice of the special meeting and to vote and have their votes counted at the special meeting and any adjournments or postponements of the special meeting.

The approval of the warrant amendment proposal is a condition to the consummation of the merger discussed above. Capitol’s officers, directors and stockholders prior to Capitol’s initial public offering, as well as Pine River, have executed lockup agreements whereby such parties have agreed to vote in favor of the warrant amendment proposal at the special meeting.

After careful consideration, Capitol’s board of directors has determined that the proposals are fair to and in the best interests of Capitol and its warrantholders and unanimously recommends that you vote or give instruction to vote “FOR” the approval of all of the proposals.

All Capitol warrantholders are cordially invited to attend the special meeting in person. To ensure your representation at the special meeting, however, you are urged to complete, sign, date and return the enclosed proxy card as soon as possible. If you are a warrantholder of record of Capitol, you may also cast your vote in person at the special meeting. If your warrants are held in an account at a brokerage firm or bank, you must instruct your broker or bank on how to vote your warrants or, if you wish to attend the meeting and vote in person, obtain a proxy from your broker or bank. If you do not vote or do not instruct your broker or bank how to vote, it will have the same effect as voting against the warrant amendment proposal.

A complete list of Capitol warrantholders of record entitled to vote at the special meeting will be available for ten days before the special meeting at the principal executive offices of Capitol for inspection by warrantholders during ordinary business hours for any purpose germane to the special meeting.

Your vote is important regardless of the number of warrants you own. Whether you plan to attend the special meeting or not, please sign, date and return the enclosed proxy card as soon as possible in the envelope provided. If your warrants are held in “street name” or are in a margin or similar account, you should contact your broker to ensure that votes related to the warrants you beneficially own are properly counted.

Thank you for your participation. We look forward to your continued support.

| , 2009 | By Order of the Board of Directors | |

| Mark D. Ein | ||

| Chairman of the Board | ||

IF YOU RETURN YOUR PROXY CARD WITHOUT AN INDICATION OF HOW YOU WISH TO VOTE, YOUR WARRANTS WILL BE VOTED IN FAVOR OF EACH OF THE PROPOSALS. IF THE MERGER IS NOT COMPLETED AND CAPITOL DOES NOT COMPLETE AN INITIAL BUSINESS COMBINATION PRIOR TO NOVEMBER 8, 2009, THEN THE WARRANTS WILL EXPIRE WORTHLESS.

The information in this proxy statement/prospectus is not complete and may be changed. We may not issue these securities until the registration statement filed with the Securities and Exchange Commission is effective. This proxy statement/prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO AMENDMENT AND COMPLETION, DATED JUNE 24, 2009

PROXY STATEMENT FOR SPECIAL MEETING OF STOCKHOLDERS AND WARRANTHOLDERS OF

CAPITOL ACQUISITION CORP.

PROSPECTUS FOR UP TO

26,249,000 SHARES OF COMMON STOCK

AND

33,249,000 WARRANTS

AND

33,249,000 SHARES OF COMMON STOCK UNDERLYING SUCH WARRANTS

OF

TWO HARBORS INVESTMENT CORP.

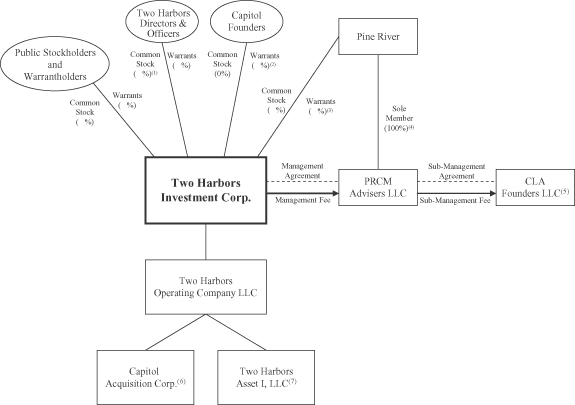

Capitol Acquisition Corp., a Delaware corporation (“Capitol”), is pleased to report that its board of directors has approved an Agreement and Plan of Merger among Capitol, Two Harbors Investment Corp., a Maryland corporation (“Two Harbors”), Two Harbors Merger Corp., a Delaware corporation (“Merger Sub Corp.”), a wholly-owned subsidiary of Two Harbors, and Pine River Capital Management L.P., a Delaware limited partnership (“Pine River”) and the sole stockholder of Two Harbors, pursuant to which (i) Merger Sub Corp. will merge with and into Capitol with Capitol surviving the merger and becoming a wholly-owned subsidiary of Two Harbors and (ii) holders of Capitol securities (not exercising conversion rights as described below) at the time of merger will be security holders of Two Harbors.

Two Harbors is a newly-formed Maryland corporation that will commence operations upon completion of the merger described in this proxy statement/prospectus. Two Harbors intends to elect and qualify to be taxed as a real estate investment trust (“REIT”) for U.S. federal income tax purposes, commencing with Two Harbors’ taxable year ending December 31, 2009. Two Harbors generally will not be subject to U.S. federal income tax on its net taxable income to the extent that it annually distributes all of its net taxable income to stockholders and maintains its intended qualification as a REIT. Two Harbors also intends to operate its business in a manner that will permit it to maintain its exemption from registration under the Investment Company Act of 1940 (“1940 Act”).

Upon consummation of the merger, Two Harbors will initially seek to invest in residential mortgage-backed securities (“RMBS”) for which a U.S. Government agency or a federally chartered corporation guarantees payments of principal and interest on the securities (“Agency RMBS”), RMBS that are not issued or guaranteed by a U.S. Government agency or federally chartered corporation (“non-Agency RMBS”) and assets other than RMBS. Two Harbors was formed solely to complete the business combination with Capitol and has no material assets or liabilities. Its only assets following the business combination will be the funds released to it from Capitol’s trust account upon consummation of the business combination and its stock of Capitol. Two Harbors will be externally managed and advised by PRCM Advisers LLC (the “Two Harbors Manager”), a subsidiary of Pine River.

Upon consummation of the merger, Capitol’s outstanding common stock and warrants will be converted into like securities of Two Harbors, on a one-to-one basis. The holders of Capitol’s common stock and warrants will be holders of the securities of Two Harbors after the merger in the same proportion as their current holdings in Capitol, except as (i) increased by (A) the cancellation of shares of common stock of Capitol by its founders immediately prior to the consummation of the merger and (B) conversion of shares of Capitol common stock sold in Capitol’s initial public offering (“Public Shares”) by any holder thereof exercising its conversion rights and (ii) decreased by the issuance of shares of restricted stock to Two Harbors’ independent directors upon consummation of the transaction, all as described in more detail in this proxy statement/prospectus.

Proposals to approve the merger agreement and the other matters discussed in this proxy statement/prospectus will be presented at the special meetings of stockholders and warrantholders of Capitol scheduled to be held on , 2009.

Capitol’s common stock, units and warrants are currently listed on the NYSE Amex under the symbols CLA, CLA.U and CLA.WS, respectively. Capitol’s units, common stock and warrants will no longer be traded following consummation of the merger. The parties intend to seek to have the common stock and warrants of Two Harbors listed on the New York Stock Exchange or the NYSE Amex following consummation of the merger under the symbols and .WS, respectively. However, there is no assurance that the common stock and warrants will be listed on any exchange following consummation of the merger.

To assist Two Harbors in qualifying as a REIT, ownership of shares of Two Harbors’ common stock by any person is limited, with certain exceptions, to 9.8% by value or by number of shares, whichever is more restrictive, of Two Harbors’ outstanding shares of common stock and no more than 9.8% by value or by number of shares, whichever is more restrictive, of Two Harbors’ outstanding capital stock. In addition, Two Harbors’ charter contains various other restrictions limiting the ownership and transfer of Two Harbors’ common stock.

Capitol is providing this proxy statement/prospectus and accompanying proxy card to its stockholders and warrantholders in connection with the solicitation of proxies to be voted at the special meetings of stockholders and warrantholders of Capitol and at any adjournments or postponements of the special meetings. Unless the context requires otherwise, references to “you” are references to Capitol stockholders and warrantholders, as the case may be, and references to “we”, “us” and “our” are to Capitol.

This proxy statement/prospectus provides you with detailed information about the merger and other matters to be considered by the Capitol stockholders and warrantholders. You are encouraged to carefully read the entire document and the documents incorporated by reference. IN PARTICULAR, YOU SHOULD CAREFULLY CONSIDER THE MATTERS DISCUSSED UNDER “RISK FACTORS” BEGINNING ON PAGE 14.

Your vote is very important. Whether or not you expect to attend the special meetings, the details of which are described on the following pages, please complete, date, sign and promptly return the accompanying proxy in the enclosed envelope.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this proxy statement/prospectus. Any representation to the contrary is a criminal offense.

The proxy statement/prospectus statement is dated , 2009, and is first being mailed on or about , 2009.

This proxy statement/prospectus incorporates important business and financial information about Capitol and Two Harbors that is not included in or delivered with this document. This information is available without charge to security holders upon written or oral request. To make this request, or if you would like additional copies of this proxy statement/prospectus or have questions about the merger, you should contact Mark D. Ein, Chief Executive Officer, Capitol Acquisition Corp., 509 7th Street, N.W., Washington, D.C. 20004, (202) 654-7060.

To obtain timely delivery of requested materials, security holders must request the information no later than five business days before the date they submit their proxies or attend the special meetings. The latest date to request the information to be received timely is , 2009.

Capitol consummated its initial public offering (“IPO”) on November 14, 2007. Citigroup Global Markets Inc. (“Citigroup”) acted as sole book-running manager and representative of the underwriters in the IPO. Upon consummation of the merger, the underwriters in Capitol’s IPO will be entitled to receive up to an aggregate of approximately $5.9 million of deferred underwriting commissions, which represents a reduction of their deferred underwriting commissions, in exchange for certain rights to participate in future securities offerings by Two Harbors following consummation of the merger. If the merger is not consummated and Capitol is required to be liquidated, the underwriters will not receive any of such funds. Capitol is having ongoing discussions with Citigroup regarding obtaining Citigroup’s consent to any necessary amendments to the agreements entered into in connection with the IPO in order to consummate the transactions described herein.

| Page | ||

| 1 | ||

| Questions and Answers For Capitol Stockholders and Warrantholders About the Proposals |

5 | |

| 10 | ||

| Selected Unaudited Pro Forma Condensed Combined Financial Information |

13 | |

| 14 | ||

| 51 | ||

| 53 | ||

| 59 | ||

| 59 | ||

| 62 | ||

| 78 | ||

| 85 | ||

| Unaudited Pro Forma Condensed Combined Financial Information |

107 | |

| 111 | ||

| 113 | ||

| 114 | ||

| 114 | ||

| 115 | ||

| 116 | ||

| 125 | ||

| 144 | ||

| 148 | ||

| Two Harbors’ Management’s Discussion and Analysis of Financial Condition and Results of Operations |

166 | |

| 179 | ||

| Certain Provisions of the Maryland General Corporation Law and Two Harbors’ Charter and Bylaws |

198 | |

| 203 | ||

| 207 | ||

| 211 | ||

| 219 | ||

| 221 | ||

| 221 | ||

| 221 | ||

| 221 | ||

| 222 | ||

| 223 | ||

| ANNEXES |

||

| A-1 | ||

| B-1 | ||

| C-1 | ||

| D-1 | ||

| E-1 | ||

| Capitol Second Amended and Restated Certificate of Incorporation |

F-1 | |

| G-1 | ||

| H-1 | ||

i

SUMMARY OF THE MATERIAL TERMS OF THE MERGER

The following summary highlights some of the information in this proxy statement/prospectus. It does not contain all of the information that you should consider before deciding how to vote on any of the proposals described herein. You should read carefully the more detailed information set forth under “Risk Factors” and the other information included in this proxy statement/prospectus.

| • | In the prospectus included in the registration statement for Capitol’s IPO, Capitol undertook to consummate an initial business combination in which it acquired an operating business with a fair market value equal to at least 80% of the balance in Capitol’s trust account (excluding deferred underwriting discounts and commissions). If the operating business was affiliated with any of Capitol’s officers, directors and stockholders prior to the IPO (“Capitol Founders”), Capitol was required to have such transaction approved by its disinterested independent directors and obtain a fairness opinion from an independent investment banking firm that the transaction was fair to public stockholders from a financial point of view. In the proposed merger, (i) Capitol will ultimately be acquired by Two Harbors, (ii) neither Two Harbors nor Merger Sub Corp. is an operating business, (iii) the fair market value of Two Harbors and Merger Sub Corp. on the date of the transaction is less than 80% of the balance of the trust account and (iv) the transaction will not be approved by disinterested independent directors (because there are no disinterested independent directors) and Capitol will not be receiving a fairness opinion from an independent investment banking firm that the transaction is fair to public stockholders from a financial point of view. Accordingly, the proposed merger does not satisfy the requirements set forth in Capitol’s amended and restated certificate of incorporation. However, Capitol considered and analyzed numerous companies and acquisition opportunities in its search for an attractive business combination candidate, none of which were believed to be as attractive to public stockholders as the proposed merger. Accordingly, Capitol is proposing to amend the terms of its amended and restated certificate of incorporation to allow for the consummation of the proposed transaction. See the section entitled “The Initial Charter Proposal.” |

| • | If the initial charter proposal is approved, stockholders will be asked to adopt the Agreement and Plan of Merger and approve the business combination contemplated by such Agreement and Plan of Merger. The parties to the Agreement and Plan of Merger are Capitol, Two Harbors, Merger Sub Corp. and Pine River. Pursuant to the agreement, (i) Merger Sub Corp. will merge with and into Capitol with Capitol surviving the merger and becoming a wholly-owned subsidiary of Two Harbors and (ii) holders of Capitol securities at the time of the merger (other than holders of Public Shares exercising conversion rights) will become security holders of Two Harbors as described below. |

| • | Two Harbors is a newly-formed Maryland corporation that will commence operations upon completion of the merger described in this proxy statement/prospectus. Two Harbors intends to elect and qualify to be taxed as a REIT for U.S. federal income tax purposes, commencing with Two Harbors’ taxable year ending December 31, 2009. Two Harbors generally will not be subject to U.S. federal income tax on its net taxable income to the extent that it annually distributes all of its net taxable income to stockholders and maintains its intended qualification as a REIT. Two Harbors also intends to operate its business in a manner that will permit it to maintain its exemption from registration under the 1940 Act. Upon consummation of the merger, Two Harbors will initially seek to invest in Agency RMBS, non-Agency RMBS and assets other than RMBS. Two Harbors was formed solely to complete the business combination with Capitol and has no material assets or liabilities. Its only assets following the business combination will be the funds released to it from Capitol’s trust account upon consummation of the business combination and its stock of Capitol. Two Harbors will be externally managed and advised by the Two Harbors Manager, a subsidiary of Pine River. Founded in 2002, Pine River is a global multi-strategy asset management firm, with approximately $800 million in assets under management as of |

| June 1, 2009, including $202 million in a private fund, Nisswa Fixed Income Master Fund Ltd. (“Nisswa Fixed Income Fund”) , dedicated to investments in RMBS and related strategies. The term |

1

| “assets under management” refers to the assets of the Pine River managed funds less the liabilities of these funds but excluding from liabilities any performance fees that have been accrued but not yet paid to Pine River. See the section entitled “Business of Two Harbors.” |

| • | As a result of the merger, the holders of common stock and warrants of Capitol will receive like securities of Two Harbors, on a one-to-one basis, in exchange for their existing Capitol securities. The holders of Capitol’s common stock and warrants will become holders of securities of Two Harbors after the merger. Pine River will not be receiving any consideration, including any shares in Two Harbors, as a result of the transaction other than a percentage of the management fees the Two Harbors Manager will be paid pursuant to the management agreement. The holders of Capitol’s common stock and warrants will own the same proportion of Two Harbors’ securities as their current holdings in Capitol, except as (i) increased by (A) the cancellation of shares of common stock of Capitol by the Capitol Founders described below and (B) any holder of Public Shares exercising its conversion rights described herein and (ii) decreased by the issuance of shares of restricted stock to Two Harbors’ independent directors upon consummation of the merger. |

| • | The merger and the transactions contemplated by the merger agreement are not subject to any additional federal or state regulatory requirement or approval, including the Hart-Scott-Rodino Antitrust Improvements Act of 1976, except for filings with the State of Delaware necessary to effectuate the merger. |

| • | Capitol has received an opinion from its counsel, Graubard Miller, relating to the tax treatment of the proposed transaction on Capitol’s stockholders and Two Harbors has received an opinion from its counsel, Clifford Chance US LLP, relating to the tax treatment of the proposed transaction on Capitol’s stockholders. Graubard Miller and Clifford Chance US LLP have consented to the use of their opinions in this proxy statement/prospectus. For a detailed description of the material U.S. federal income tax consequences of the merger and warrant amendment, see the section entitled “U.S. Federal Income Tax Considerations.” |

| • | In connection with the merger, the Capitol Founders have agreed to have cancelled the 6,562,257 shares (“Founders’ Shares”) acquired by them prior to the IPO. |

| • | Concurrent with the consummation of the merger, Two Harbors will enter into a management agreement with the Two Harbors Manager pursuant to which the Two Harbors Manager will provide the day-to-day management of Two Harbors’ operations. The management agreement requires the Two Harbors Manager to manage Two Harbors’ business affairs in conformity with the policies and the investment guidelines that are approved and monitored by Two Harbors’ board of directors. The management agreement has an initial three-year term and will be renewed for one-year terms thereafter unless terminated by either Two Harbors or the Two Harbors Manager. The Two Harbors Manager is entitled to receive from Two Harbors a management fee, payable quarterly in arrears equal to 1.5% of Two Harbors’ stockholder equity (as defined in the management agreement). Two Harbors is also obligated to reimburse certain expenses incurred by the Two Harbors Manager and its affiliates. The Two Harbors Manager is further entitled to receive a termination fee from Two Harbors under certain circumstances. For a more detailed description of the management agreement, see the section entitled “Management of Two Harbors Following the Merger.” |

| • | CLA Founders LLC, an entity affiliated with the Capitol Founders (“Sub-Manager”), has agreed to provide certain services to the Two Harbors Manager upon consummation of the merger pursuant to a sub-management agreement. In exchange for such services, Sub-Manager will receive a sub-management fee of 20% of the management fee earned by the Two Harbors Manager under its management agreement with Two Harbors with respect to the first $1 billion of Two Harbors’ stockholders’ equity and 10% of the management fee earned by the Two Harbors Manager under the management agreement with respect to Two Harbors’ stockholders’ equity in excess of $1 billion. |

2

| • | Unless terminated earlier, the sub-management agreement will terminate on the fifth anniversary of the merger, at which time Sub-Manager will be paid a final payment equal to 7.7 times the annualized rate of the last quarterly payment to Sub-Manager, subject to certain adjustments. The sub-management agreement provides that, during its five year term, if the Two Harbors Manager or certain Pine River affiliates manage certain other public investment vehicles, including other REITs, the Two Harbors Manager will negotiate in good faith to provide Sub-Manager the right to enter into a sub-management agreement on substantially the same terms as the sub-management agreement or an alternative arrangement reasonably acceptable to the Two Harbors Manager and Sub-Manager. For a more detailed description of the interests of the Capitol Founders and other persons having an interest in the transaction, see the section entitled “The Merger Proposal — Interests of Capitol’s Directors and Officers and Others in the Merger.” |

| • | It is possible that the present holders of 30.0% or more of the Public Shares will vote against the merger and seek conversion of their Public Shares into cash in accordance with Capitol’s amended and restated certificate of incorporation. If such event were to occur, the merger could not be completed. To preclude such possibility Capitol, the Capitol Founders, Two Harbors and their respective affiliates may enter into arrangements to provide for the purchase of the Public Shares from holders thereof who indicate their intention to vote against the merger and seek conversion or otherwise wish to sell their Public Shares or other arrangements that would induce holders of Public Shares not to vote against the merger proposal. Definitive arrangements have not yet been determined but some possible methods are described in the section titled “The Merger Proposal — Actions That May Be Taken to Secure Approval of Capitol’s Stockholders.” |

| • | At the closing of the merger, the funds in Capitol’s trust account will be released to pay transaction fees and expenses, deferred underwriting discounts and commissions, tax liabilities and reimbursement of expenses of the Capitol Founders and to make purchases of Public Shares, if any. The balance of the funds will be released to Two Harbors to pay Capitol stockholders who properly exercise their conversion rights and for working capital and general corporate purposes of Two Harbors and Capitol. The merger is conditioned on Capitol’s trust account containing no less than $100 million after the closing after taking into account all of the payments described above. |

| • | After the merger, the directors of Two Harbors will be Brian C. Taylor, Thomas Siering, , and , who are designees of Pine River, and Mark D. Ein and , who are designees of Capitol. , , and will be considered independent directors under applicable regulatory rules. The officers of Two Harbors will be Thomas Siering, Steven Kuhn, William Roth, Jeffrey Stolt, Andrew Garcia and Timothy O’Brien. |

| • | In addition to voting on the initial charter proposal and the merger proposal, the stockholders of Capitol will vote on proposals to: |

| • | approve the following differences between the charter of Two Harbors to be in effect following the merger and Capitol’s amended and restated certificate of incorporation: (i) the name of the new public entity will be “Two Harbors Investment Corp.” as opposed to “Capitol Acquisition Corp.”; (ii) Two Harbors will have 450,000,000 authorized shares of common stock and 50,000,000 authorized shares of preferred stock and may increase or decrease such amounts without stockholder approval, as opposed to Capitol having 75,000,000 authorized shares of common stock and 1,000,000 authorized shares of preferred stock and not being able to increase or decrease such amounts without stockholder approval; (iii) Two Harbors’ corporate existence will be perpetual as opposed to Capitol’s corporate existence terminating on November 8, 2009; (iv) Two Harbors’ board of directors will not be classified as opposed to Capitol’s which is classified; (v) Two Harbors’ charter will not include the various provisions applicable only to |

3

| specified purpose acquisition corporations that Capitol’s amended and restated certificate of incorporation contains; and (vi) Two Harbors’ charter will include various provisions relating to Two Harbors’ intention to elect and qualify to be taxed as a REIT for U.S. federal income tax purposes, commencing with Two Harbors’ taxable year ending December 31, 2009, which are not included in Capitol’s amended and restated certificate of incorporation. Under the merger agreement, the approval of the secondary charter proposals is not a condition to the consummation of the merger and the vote on such proposal will not impact whether the merger is consummated. See the section entitled “The Secondary Charter Proposals.” |

| • | adjourn the meeting, if necessary. It is possible for Capitol to obtain sufficient votes to approve the adjournment proposal but not receive sufficient votes to approve the initial charter proposal and merger proposal. In such a situation, Capitol could adjourn the meeting and attempt to solicit additional votes in favor of such proposals. See the section entitled “The Adjournment Proposal.” |

| • | Capitol is also seeking the approval from the holders of its warrants to (i) increase the exercise price of Capitol’s warrants from $7.50 per share to $11.00 per share and (ii) extend the expiration date of the warrants from November 7, 2012 to November 7, 2013. The approval of the warrant amendment proposal is a condition to the merger being consummated. The amendments will be effective immediately upon consummation of the merger. The Capitol Founders, as well as Pine River, have executed lockup agreements whereby such parties have agreed to vote in favor of the warrant amendment proposal at the special meeting. See the section entitled “The Warrant Amendment Proposal.” |

| • | In evaluating the proposals described above, you should carefully read this proxy statement/prospectus and especially consider the factors discussed in the section entitled “Risk Factors.” |

4

FOR CAPITOL STOCKHOLDERS AND WARRANTHOLDERS ABOUT THE PROPOSALS

| Q. | Why am I receiving this proxy statement/prospectus? | A. Capitol has agreed to a business combination under the terms of the Agreement and Plan of Merger that is described in this proxy statement/prospectus. This agreement is referred to as the merger agreement. A copy of the merger agreement is attached to this proxy statement/prospectus as Annex A, which you are encouraged to read.

Stockholders are being asked to consider and vote upon proposals entitled “Initial Charter Proposal,” “The Merger Proposal,” “The Secondary Charter Proposals” and “The Adjournment Proposal,” all as described in more detail in this proxy statement/prospectus. Warrantholders are being asked to consider and vote upon proposals entitled “The Warrant Amendment Proposal” and “The Adjournment Proposal,” all as described in more detail in this proxy statement/prospectus.

The approval of the initial charter proposal, the merger proposal and the warrant amendment proposal is a condition to the consummation of the merger. If either the initial charter proposal, the merger proposal or the warrant amendment proposal is not approved, the other proposals will not be presented to stockholders and warrantholders for a vote and the merger will not be consummated.

This proxy statement/prospectus contains important information about the proposed merger and the other matters to be acted upon at the special meetings. You should read it carefully.

Your vote is important. You are encouraged to vote as soon as possible after carefully reviewing this proxy statement/prospectus. | ||

| Q. | Do I have conversion rights? | A. If you are a holder of Public Shares, you have the right to vote against the merger proposal and demand that Capitol convert such shares into a pro rata portion of the trust account in which a substantial portion of the net proceeds of Capitol’s IPO are held. These rights to vote against the merger and demand conversion of the Public Shares into a pro rata portion of the trust account are sometimes referred to herein as conversion rights. | ||

| Q. | How do I exercise my conversion rights? | A. If you are a holder of Public Shares and wish to exercise your conversion rights, you must (i) vote against the merger proposal, (ii) demand that Capitol convert your shares into cash, and (iii) deliver your stock to Capitol’s transfer agent physically or electronically using the Depository Trust Company’s DWAC (Deposit Withdrawal at Custodian) System prior to the vote at the meeting.

Any action that does not include an affirmative vote against the merger will prevent you from exercising your conversion rights. Your vote on any proposal other than the merger proposal will have no impact on your right to convert.

You may exercise your conversion rights either by checking the box on the proxy card or by submitting your request in writing to Mark Zimkind of Continental Stock Transfer & Trust Company, Capitol’s transfer agent, at the address listed at the end of this section. If you (i) initially vote for the merger proposal but then wish to vote against it and exercise your conversion rights or (ii) initially vote against the merger proposal and wish to exercise your conversion rights but do not check the box on the proxy card providing for the exercise of your conversion rights or do not send a written request to Capitol to exercise your conversion rights, or (iii) initially vote against the merger but later wish to vote for it, you may request Capitol to send you another proxy card on which you may indicate your | ||

5

| intended vote. You may make such request by contacting Capitol at the phone number or address listed at the end of this section.

Any request for conversion, once made, may be withdrawn at any time up to the vote taken with respect to the merger proposal. If you delivered your shares for conversion to Capitol’s transfer agent and decide prior to the special meeting not to elect conversion, you may request that Capitol’s transfer agent return the shares (physically or electronically). You may make such request by contacting Capitol’s transfer agent at the phone number or address listed at the end of this section.

Any corrected or changed proxy card must be received by Capitol’s secretary prior to the special meeting. No demand for conversion will be honored unless the holder’s stock has been delivered (either physically or electronically) to the transfer agent prior to the meeting.

If the merger is completed, then, if you have also properly exercised your conversion rights, you will be entitled to receive a pro rata portion of the trust account, including any interest earned thereon, calculated as of two business days prior to the date of the consummation of the merger. As of March 31, 2009, there was $259,094,847 in the trust account, which would amount to approximately $9.87 per Public Share upon conversion. If you exercise your conversion rights, then you will be exchanging your shares of Capitol common stock for cash and will no longer own these shares.

Exercise of your conversion rights does not result in either the exercise or loss of any Capitol warrants that you may hold. Your warrants will continue to be outstanding following a conversion of your common stock, will be automatically converted into warrants to purchase shares of Two Harbors’ common stock that will have terms that are substantially similar in all material respects to those of the Capitol warrants (subject to the amendments to the warrants contemplated by the warrant amendment proposal) and will become exercisable upon consummation of the merger. A registration statement must be in effect to allow you to exercise any warrants you may hold or to allow Two Harbors to call the warrants for redemption if the redemption conditions are satisfied. If the merger is not consummated and Capitol does not complete a different business combination prior to November 8, 2009, the warrants will not become exercisable and will be worthless upon dissolution of Capitol in accordance with its charter. | ||||

| Q. | Do I have appraisal rights if I object to the proposed merger? | A No. Neither Capitol stockholders nor warrantholders have appraisal rights in connection with the merger. | ||

| Q. | What happens to the funds deposited in the trust account after consummation of the merger? | A. At the closing of the merger, the funds in the trust account will be released to pay transaction fees and expenses, deferred underwriting discounts and commissions, tax liabilities and reimbursement of expenses of the Capitol Founders and to make purchases of Public Shares, if any. The balance of the funds will be released to Two Harbors to pay Capitol stockholders who properly exercise their conversion rights and for working capital and general corporate purposes of Two Harbors and Capitol. The merger is conditioned on Capitol’s trust account containing no less than $100 million after the closing after taking into account all of the payments described above. | ||

6

| Q. | Since Capitol’s IPO prospectus contained certain differences in what is being proposed at the meeting, what are my legal rights? | A. You should be aware that Capitol’s amended and restated certificate of incorporation and IPO prospectus require Capitol to complete a business combination in which it acquires a target business having a fair market value equal to at least 80% of Capitol’s trust account balance (excluding deferred underwriting discounts and commissions) and, if the transaction is a related party transaction, to obtain the approval from disinterested independent directors and an opinion from an independent investment banking firm indicating that the transaction is fair to public stockholders from a financial point of view. Furthermore, Capitol’s IPO prospectus did not disclose that funds in its trust account might be used, directly or indirectly, to purchase Public Shares other than from holders who have indicated their intention to vote against the merger and seek conversion of their shares to cash (as Capitol may contemplate doing). Also, Capitol’s IPO prospectus stated that specific provisions in Capitol’s amended and restated certificate of incorporation may not be amended prior to the consummation of an initial business combination but that Capitol had been advised that such provision limiting its ability to amend its amended and restated certificate of incorporation may not be enforceable under Delaware law. Accordingly, each holder of Public Shares at the time of the merger who purchased such shares in the IPO and still held them at the time of the merger without seeking to convert them into cash may have securities law claims against Capitol for rescission (under which a successful claimant has the right to receive the total amount paid for his or her securities pursuant to an allegedly deficient prospectus, plus interest and less any income earned on the securities, in exchange for surrender of the securities) or damages (compensation for loss on an investment caused by alleged material misrepresentations or omissions in the sale of a security).

Such claims may entitle stockholders asserting them to as much as $10.00 or more per share, based on the initial offering price of the IPO units comprised of stock and warrants, less any amount received from sale of the original warrants, plus interest from the date of Capitol’s IPO (which, in the case of holders of Public Shares, may be more than the pro rata share of the trust account to which they are entitled on conversion or liquidation). See “The Merger Proposal — Rescission Rights.” | ||

| Q. | What happens if the merger is not consummated? | A. If the merger is not consummated by September 8, 2009, subject to extension in certain instances, either party may terminate the merger agreement. If Capitol is unable to complete the merger or another business combination by November 8, 2009, its amended and restated certificate of incorporation provides that it must liquidate. In any liquidation of Capitol, the funds deposited in the trust account, plus any interest earned thereon and remaining in trust, less claims requiring payment from the trust account by creditors who have not waived their rights against the trust account, if any, will be distributed pro rata to the holders of Capitol’s Public Shares. Holders of the Founders’ Shares, including all of Capitol’s officers and directors, have waived any right to any liquidation distribution with respect to those shares. Mark D. Ein, Capitol’s Chief Executive Officer, has agreed to be personally liable under certain circumstances to ensure that the proceeds in the trust account are not reduced by the claims of prospective target businesses and vendors or other entities that are owed money by Capitol for services rendered or products sold to it. Capitol cannot assure you that Mr. Ein will be able to satisfy those obligations. See the section entitled “Other Information Related to Capitol —Liquidation If No Business Combination” for additional information. | ||

7

| Q. | When do you expect the merger to be completed? | A. It is currently anticipated that the merger will be consummated promptly following the Capitol special meetings on , 2009.

For a description of the conditions for the completion of the merger, see the section entitled “The Merger Agreement — Conditions to Closing of the Merger.” | ||

| Q. | What do I need to do now? | A. Capitol urges you to read carefully and consider the information contained in this proxy statement/prospectus, including the annexes, and to consider how the merger, warrant amendment and other proposals will affect you as a stockholder or warrantholder of Capitol. You should then vote as soon as possible in accordance with the instructions provided in this proxy statement/prospectus and on the enclosed proxy card. | ||

| Q. | How do I vote? | A. If you are a holder of record of Capitol common stock or warrants, you may vote in person at the special meetings or by submitting a proxy for the special meetings. You may submit your proxy by completing, signing, dating and returning the enclosed proxy card in the accompanying pre-addressed postage paid envelope. If you hold your shares or warrants in “street name,” which means your shares or warrants are held of record by a broker, bank or nominee, you should contact your broker to ensure that votes related to the shares or warrants you beneficially own are properly counted. In this regard, you must provide the record holder of your shares or warrants with instructions on how to vote your shares or warrants or, if you wish to attend the meetings and vote in person, obtain a proxy from your broker, bank or nominee. | ||

| Q. | If my shares or warrants are held in “street name,” will my broker, bank or nominee automatically vote my shares or warrants for me? | A. No. Your broker, bank or nominee cannot vote your shares or warrants unless you provide instructions on how to vote in accordance with the information and procedures provided to you by your broker, bank or nominee. | ||

| Q. | May I change my vote after I have mailed my signed proxy card? | A. Yes. Send a later-dated, signed proxy card to Capitol’s secretary at the address set forth below so that it is received by Capitol’s secretary prior to the special meetings or attend the special meetings in person and vote. You also may revoke your proxy by either sending a notice of revocation to Capitol’s secretary, which must be received by Capitol’s secretary prior to the special meetings, or attending the special meetings and revoking your proxy and voting in person. | ||

| Q. | What should I do with my stock, warrant and unit certificates? | A. Upon consummation of the merger, Capitol’s units will automatically separate and no longer be traded as a separate security.

If you are not electing conversion in connection with your vote on the merger proposal, the merger is approved and consummated, and you hold your securities in Capitol in certificate form, as opposed to holding your securities through your broker, you do not need to exchange your existing certificates for certificates issued by Two Harbors. Your current Capitol certificates will automatically represent your rights in Two Harbors’ securities. You may, however, exchange your certificates if you choose, by contacting Two Harbors’ transfer agent, | ||

8

| Continental Stock Transfer & Trust Company (Reorganization Department), after the consummation of the merger and following their requirements for reissuance.

Capitol stockholders who affirmatively vote against the merger and exercise their conversion rights must deliver their shares to Capitol’s transfer agent (either physically or electronically) as instructed by Capitol or Capitol’s transfer agent prior to the vote at the meeting. | ||||

| Q. | What should I do if I receive more than one set of voting materials? | A. You may receive more than one set of voting materials, including multiple copies of this proxy statement/prospectus and multiple proxy cards or voting instruction cards. For example, if you hold your shares or warrants in more than one brokerage account, you will receive a separate voting instruction card for each brokerage account in which you hold shares or warrants. If you are a holder of record and your shares or warrants are registered in more than one name, you will receive more than one proxy card. Please complete, sign, date and return each proxy card and voting instruction card that you receive in order to cast a vote with respect to all of your Capitol shares or warrants. | ||

| Q. | Who can help answer my questions? | A. If you have questions about the merger or if you need additional copies of the proxy statement/prospectus or the enclosed proxy card you should contact:

Mr. Mark D. Ein Capitol Acquisition Corp. 509 7th Street, N.W. Washington, D.C. 20004 Tel: (202) 654-7060 Fax: (202) 654-7063

or

[Proxy solicitation firm]

You may also obtain additional information about Capitol from documents filed with the Securities and Exchange Commission (“SEC”) by following the instructions in the section entitled “Where You Can Find More Information.”

If you intend to affirmatively vote against the merger and seek conversion of your shares, you will need to deliver your stock (either physically or electronically) to Capitol’s transfer agent prior to the vote at the meeting. If you have questions regarding the certification of your position or delivery of your stock, please contact:

Mr. Mark Zimkind Continental Stock Transfer & Trust Company 17 Battery Place New York, New York 10004 Tel: (212) 845-3287 Fax: (212) 616-7616 | ||

9

SELECTED HISTORICAL CONSOLIDATED FINANCIAL INFORMATION

Capitol and Two Harbors are providing the following selected historical financial information to assist you in your analysis of the financial aspects of the merger.

Two Harbors’ balance sheet data as of June 11, 2009 are derived from Two Harbors’ audited balance sheet, which is included elsewhere in this proxy statement/prospectus.

Capitol’s balance sheet data as of December 31, 2008 and December 31, 2007 and statements of income data and cash flow data for the year ended December 31, 2008, and for the period from June 26, 2007 (inception) through December 31, 2007 and 2008 are derived from Capitol’s audited financial statements, which are included elsewhere in this proxy statement/prospectus. Capitol’s balance sheet data as of March 31, 2009 and statements of income data and cash flow data for the three months ended March 31, 2009 and 2008 are derived from Capitol’s unaudited financial statements, which are included elsewhere in this proxy statement/prospectus.

The information is only a summary and should be read in conjunction with each of Capitol’s and Two Harbors’ historical financial statements and related notes and “Other Information Related to Capitol — Capitol’s Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Two Harbors’ Management’s Discussion and Analysis of Financial Condition and Results of Operations” contained elsewhere herein. The historical results included below and elsewhere in this proxy statement/prospectus are not indicative of the future performance of Two Harbors.

10

SELECTED HISTORICAL CONSOLIDATED FINANCIAL INFORMATION — TWO HARBORS

| June 11, 2009 | |||

| Balance Sheet Data: |

|||

| Total Assets |

$ | 1,001 | |

| Total Liabilities |

$ | 1 | |

| Total Stockholders’ Equity |

$ | 1,000 | |

| Net Asset Value Per Share |

$ | 1.00 | |

11

SELECTED HISTORICAL FINANCIAL INFORMATION — CAPITOL

| For the Three Months Ended March 31, |

For the Year Ended December 31, 2008 |

For the Period From June 26, 2007 (inception) through December 31, 2007 |

||||||||||||||

| Income Statement Data: |

2009 | 2008 | ||||||||||||||

| (Unaudited) | ||||||||||||||||

| Revenue |

$ | — | $ | — | $ | — | $ | — | ||||||||

| Loss from operations |

(320,402 | ) | (284,012 | ) | (1,059,606 | ) | (140,999 | ) | ||||||||

| Interest and dividend income |

48,247 | 2,234,809 | 4,442,222 | 1,474,220 | ||||||||||||

| Net (loss) income attributable to common stockholders |

$ | (211,005 | ) | $ | 1,287,526 | $ | 2,058,827 | $ | 714,573 | |||||||

| Basic and diluted net (loss) income per share |

$ | (0.01 | ) | $ | 0.05 | $ | 0.08 | $ | 0.06 | |||||||

| Weighted average shares outstanding excluding shares subject to possible conversion — basic and diluted |

24,936,558 | 24,936,558 | 24,936,558 | 11,602,789 | ||||||||||||

| Balance Sheet Data: |

March 31, 2009 | December 31, 2008 | December 31, 2007 | ||||||

| Working capital |

$ | 2,486,304 | $ | 2,769,263 | $ | 1,260,417 | |||

| Trust account, restricted |

$ | 259,094,847 | $ | 259,084,043 | $ | 258,346,625 | |||

| Total assets |

$ | 261,864,221 | $ | 262,095,130 | $ | 260,303,897 | |||

| Total liabilities |

$ | 142,814 | $ | 193,555 | $ | 696,855 | |||

| Value of common stock which may be redeemed for cash ($9.87, $9.87, and $9.84 per share, respectively) |

$ | 77,770,521 | $ | 77,739,684 | $ | 77,503,978 | |||

| Stockholders’ equity |

$ | 183,950,886 | $ | 184,161,891 | $ | 182,103,064 | |||

| For the Three Months Ended March 31, |

For the Year Ended December 31, 2008 |

For the Period From June 26, 2007 (inception) through December 31, 2007 |

||||||||||||||

| Cash Flow Data: |

2009 | 2008 | ||||||||||||||

| (Unaudited) | ||||||||||||||||

| Net cash (used in) provided by operating activities |

$ | (200,091 | ) | $ | 1,283,542 | $ | 1,763,031 | $ | 1,389,340 | |||||||

| Net cash (used in) provided by investing activities |

$ | (5,849 | ) | $ | (396,060 | ) | $ | 554,148 | $ | (259,820,845 | ) | |||||

| Net cash (used in) provided by financing activities |

$ | — | $ | — | $ | (511 | ) | $ | 258,892,980 | |||||||

| Net (decrease) increase in cash |

$ | (205,940 | ) | $ | 887,482 | $ | 2,316,668 | $ | 461,475 | |||||||

12

SELECTED UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL INFORMATION

The selected unaudited pro forma condensed combined financial information has been derived from, and should be read in conjunction with, the unaudited pro forma condensed combined financial information included elsewhere in this proxy statement/prospectus.

The unaudited pro forma condensed combined balance sheet as of March 31, 2009 gives pro forma effect to the merger as if it had occurred on such date. The unaudited pro forma condensed combined balance sheet at March 31, 2009 was derived from Capitol’s unaudited condensed financial statements and Two Harbors’ audited financial statements as of March 31, 2009 and June 11, 2009, respectively.

The historical financial information has been adjusted to give effect to pro forma events that are related and/or directly attributable to the merger and are factually supportable. The adjustments presented on the unaudited pro forma condensed combined financial information have been identified and presented in “Unaudited Pro Forma Condensed Combined Financial Data” to provide relevant information necessary for an accurate understanding of the combined company upon consummation of the merger.

This information should be read together with the consolidated financials statements of Capitol and the notes thereto, the financial statements of Two Harbors and the notes thereto, “Unaudited Pro Forma Condensed Combined Financial Data,” “Capitol’s Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and “Two Harbors’ Management’s Discussion and Analysis of Financial Condition and Results of Operations” included elsewhere in this proxy statement/prospectus.

The unaudited pro forma condensed combined financial statements have been prepared using the assumptions below with respect to cash and stockholders’ equity:

| • | Assuming Minimum Conversion: This presentation assumes that no Capitol stockholders exercise conversion rights with respect to their shares of Capitol common stock into a pro rata portion of the trust account and that all of the funds held in the trust account are available after closing for the payment of transactional costs and for operating purposes; and |

| • | Assuming Maximum Conversion: This presentation assumes that pursuant to the merger proposal, Capitol stockholders holding 30.0% of the Public Shares exercise their conversion rights, such shares were converted into their pro rata share of the funds in the trust account, and/or Capitol takes actions to secure approval of the merger proposal as described in the section titled “The Merger Proposal — Actions That May be Taken to Secure Approval of Capitol’s Stockholders,” and Capitol’s trust account contains $100 million at the closing. |

The unaudited pro forma condensed combined financial statements are presented for informational purposes only and are subject to a number of uncertainties and assumptions and do not purport to represent what the companies’ actual performance or financial position would have been had the transaction occurred on the dates indicated and does not purport to indicate the financial position or results of operations as of any future date or for any future period.

Two Harbors Investment Corp. and Subsidiaries Unaudited Pro Forma

Balance Sheet Data at March 31, 2009

| Combined Pro Forma (assuming no conversion) |

Combined Pro Forma (assuming maximum conversion) | |||||

| Cash |

$ | 248,896,789 | $ | 100,001,000 | ||

| Total Current Assets |

$ | 248,916,261 | $ | 100,020,472 | ||

| Total Assets |

$ | 249,056,518 | $ | 100,160,729 | ||

| Total Current Liabilities |

$ | 142,815 | $ | 142,815 | ||

| Total Stockholders’ Equity |

$ | 248,913,703 | $ | 100,017,914 | ||

13

You should carefully consider the following risk factors, together with all of the other information included in this proxy statement/prospectus, before you decide whether to vote or instruct your vote to be cast to approve the proposals described in this proxy statement/prospectus.

Risks Related to Two Harbors’ Business and Operations Following the Merger

The value of your investment in Two Harbors following consummation of the merger will be subject to the significant risks affecting REITs, and mortgage REITs in particular, described below. If any of the events described below occur, Two Harbors’ post-acquisition business, financial condition, liquidity and/or results of operations could be adversely affected in a material way. This could cause the price of its common stock or warrants to decline, perhaps significantly, and you therefore may lose all or part of your investment.

Risks Related To Two Harbors’ Business

Two Harbors operates in a highly competitive market and competition may limit its ability to acquire desirable assets.

Two Harbors operates in a highly competitive market. Two Harbors’ profitability depends, in large part, on its ability to acquire its target assets at favorable prices. In acquiring its target assets, Two Harbors will compete with a variety of institutional investors, including other REITs, specialty finance companies, public and private funds, commercial and investment banks, commercial finance and insurance companies and other financial institutions. Many of Two Harbors’ competitors are substantially larger and have considerably greater financial, technical, marketing and other resources than Two Harbors does. Other REITs may raise significant amounts of capital, and may have investment objectives that overlap with Two Harbors’, which may create additional competition for opportunities to acquire assets. Some competitors may have a lower cost of funds and access to funding sources that may not be available to Two Harbors, such as funding from the U.S. government, if Two Harbors is not eligible to participate in certain programs established by the U.S. government. Many of Two Harbors’ competitors are not subject to the operating constraints associated with REIT qualification or maintenance of an exemption from the 1940 Act. In addition, some of Two Harbors’ competitors may have higher risk tolerances or different risk assessments, which could allow them to consider a wider variety of assets and establish more relationships than Two Harbors. Furthermore, competition for assets of the types and classes which Two Harbors will seek to acquire may lead to the price of such assets increasing, which may further limit its ability to generate desired returns. Two Harbors cannot assure you that the competitive pressures Two Harbors faces will not have a material adverse effect on its business, financial condition and results of operations. Also, as a result of this competition, desirable assets may be limited in the future and Two Harbors may not be able to take advantage of attractive opportunities from time to time, as Two Harbors can provide no assurance that Two Harbors will be able to identify and make acquisitions that are consistent with its objectives.

Two Harbors has no operating history and may not be able to successfully operate its business or generate sufficient revenue to make or sustain distributions to its stockholders.

Two Harbors was incorporated in May 2009 and has no operating history. Two Harbors has no assets and will commence operations only upon consummation of the merger. Two Harbors cannot assure you that it will be able to operate its business successfully or implement its policies and strategies as described in this proxy statement/prospectus. The results of its operations depend on several factors, including the availability of opportunities for the acquisition of assets, the level and volatility of interest rates, the availability of adequate short and long-term financing, conditions in the financial markets and economic conditions. Additionally, the past performance of the Two Harbors Manager’s affiliates, including the Nisswa Fixed Income Fund, should not be viewed as an indication of the future performance of Two Harbors. There can be no guarantee that Two

14

Harbors will have similar opportunities to invest in assets that generate similar returns. Further, differences between the structure, term and investment objectives and policies of Two Harbors and the Two Harbors Manager’s affiliates may affect their respective returns.

Two Harbors may change any of its strategies, policies or procedures without stockholder consent.

Two Harbors may change any of its strategies, policies or procedures with respect to acquisitions, asset allocation, growth, operations, indebtedness, financing strategy and distributions at any time without the consent of its stockholders, which could result in its making acquisitions that are different from, and possibly riskier than, the types of acquisitions described in this proxy statement/prospectus. A change in its strategy may increase its exposure to credit risk, interest rate risk, financing risk, default risk and real estate market fluctuations. Furthermore, a change in its asset allocation could result in its making acquisitions in asset categories different from those described in this proxy statement/prospectus. These changes could adversely affect its financial condition, results of operations, the market price of its common stock or warrants and its ability to make distributions to its stockholders.

Difficult conditions in the mortgage and residential real estate markets may cause Two Harbors to experience market losses related to its holdings, and Two Harbors does not expect these conditions to improve in the near future.

Two Harbors’ results of operations are materially affected by conditions in the mortgage market, the residential real estate market, the financial markets and the economy generally. Recently, concerns about the mortgage market and a declining real estate market, as well as inflation, energy costs, geopolitical issues and the availability and cost of credit, have contributed to increased volatility and diminished expectations for the economy and markets going forward. The mortgage market, including the market for mortgage loans that generally conform to Agency underwriting guidelines (“Prime Mortgage Loans”) and mortgage loans made to borrowers whose qualifying mortgage characteristics do not conform to Agency underwriting guidelines and generally allow homeowners to qualify for a mortgage loan with reduced or alternate forms of documentation (“Alt-A Mortgage Loans”), has been severely affected by changes in the lending landscape and there is no assurance that these conditions have stabilized or that they will not worsen. The severity of the liquidity limitation was largely unanticipated by the markets. For now (and for the foreseeable future), access to mortgages has been substantially limited. While the limitation on financing was initially in the sub-prime mortgage market, the liquidity issues have now also affected prime and Alt-A non-Agency lending, with lending standards significantly more stringent than in recent periods and many product types being severely curtailed. This has an impact on new demand for homes, which will compress the home ownership rates and weigh heavily on future home price performance. There is a strong correlation between home price growth rates and mortgage loan delinquencies. The further deterioration of the market for RMBS may cause Two Harbors to experience losses related to its assets and to sell assets at a loss. Declines in the market values of its investments may adversely affect its results of operations and credit availability, which may reduce earnings and, in turn, cash available for distribution to its stockholders.

Dramatic declines in the housing market, with falling home prices and increasing foreclosures and unemployment, have resulted in significant asset write-downs by financial institutions, which have caused many financial institutions to seek additional capital, to merge with other institutions and, in some cases, to fail. Institutions from which Two Harbors may seek to obtain financing may have owned or financed residential mortgage loans, real estate-related securities and real estate loans, which have declined in value and caused them to suffer losses as a result of the recent downturn in the residential mortgage market. Many lenders and institutional investors have reduced and, in some cases, ceased to provide funding to borrowers, including other financial institutions. If these conditions persist, these institutions may become insolvent or tighten their lending standards, which could make it more difficult for Two Harbors to obtain financing on favorable terms or at all. Two Harbors’ profitability may be adversely affected if it is unable to obtain cost-effective financing for its assets.

15

The lack of liquidity of Two Harbors’ assets may adversely affect Two Harbors’ business, including its ability to value and sell its assets.